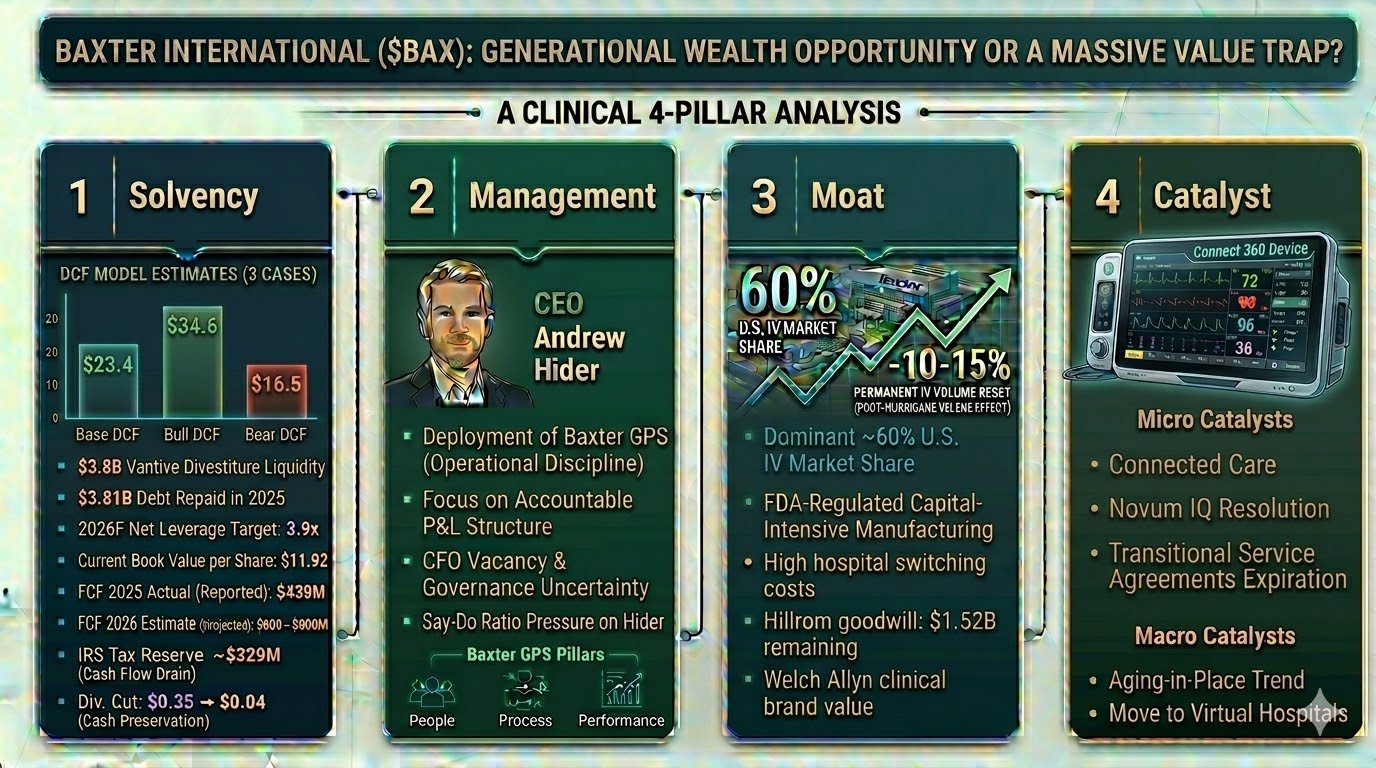

The "New Baxter" Strategic Context

Baxter International BAX$15.92-0.31% currently represents a high-conviction deep-value play, predicated on a clinical assessment of its asymmetrical risk-to-reward profile following the February 12, 2026, share price collapse. The 16% single-session plunge was catalyzed by a "perfect storm" in Q4 2025: while Baxter delivered a solid 8% revenue beat (2.97 billion), this was undermined by a staggering 17.8% EPS miss ($0.44 vs. $0.53 expected). Most critically for the forward-looking thesis, adjusted gross margins compressed by nearly 900 basis points, driven by manufacturing inefficiencies and a structural shift in product mix.

The "So What?" for institutional investors lies in the valuation anchor: Baxter currently trades at a generational low of 0.8x sales, a massive discount to the MedTech peer average of >5x. This valuation gap persists as Baxter attempts a painful pivot from its legacy kidney care business (Vantive) toward a high-tech MedTech entity focused on "Connected Care." While the market has reacted with extreme skepticism, the 45% one-year decline has created a potential floor for deep-value entry, provided the company can stabilize its foundational financial health.

Pillar 1: Solvency

In a high-leverage turnaround, solvency is the primary defense against permanent capital loss. Baxter is currently navigating an aggressive deleveraging mandate necessitated by the $10.5 billion Hillrom acquisition in 2021. The $3.8 billion Vantive divestiture to Carlyle Group provided a critical liquidity injection, allowing the repayment of $3.81 billion in debt during 2025 and clearing the 2026 maturity wall.

Capital Structure Evolution (2023–2026F)

| Metric | 2023 Actual | 2024 Actual | 2025 Actual | 2026 Forecast |

| Total Debt (Reported) | $13.73B | $13.11B | $9.78B | $7.98B (Target) |

| Total Shareholder Equity | $8.47B | $7.02B | $6.10B | $8.71B |

| Cash & Equivalents | $3.19B | $1.76B | $1.97B | $2.67B |

| Net Leverage Ratio | 4.1x | 6.2x | 4.1x | 3.9x (Forecast) |

| Dividend per Share | $0.68 | $0.68 | $0.35 | $0.04 |

Note: 2026 forecast leverage reflects S&P Global estimates.

Credit risk remains the central headwind. While Moody’s ('Baa3') and S&P ('BBB-') maintain investment-grade ratings, the outlook is negative. S&P has set a firm 3.75x downgrade threshold; current projections suggest Baxter may hit 3.9x in 2026, placing its rating in the "danger zone." A move to speculative grade would materially spike refinancing costs for the remaining 9.5 billion debt stack. Furthermore, an opaque **329 million IRS tax reserve** related to transfer pricing in Costa Rica and Puerto Rico represents a significant cash-flow drain that competes directly with debt retirement.

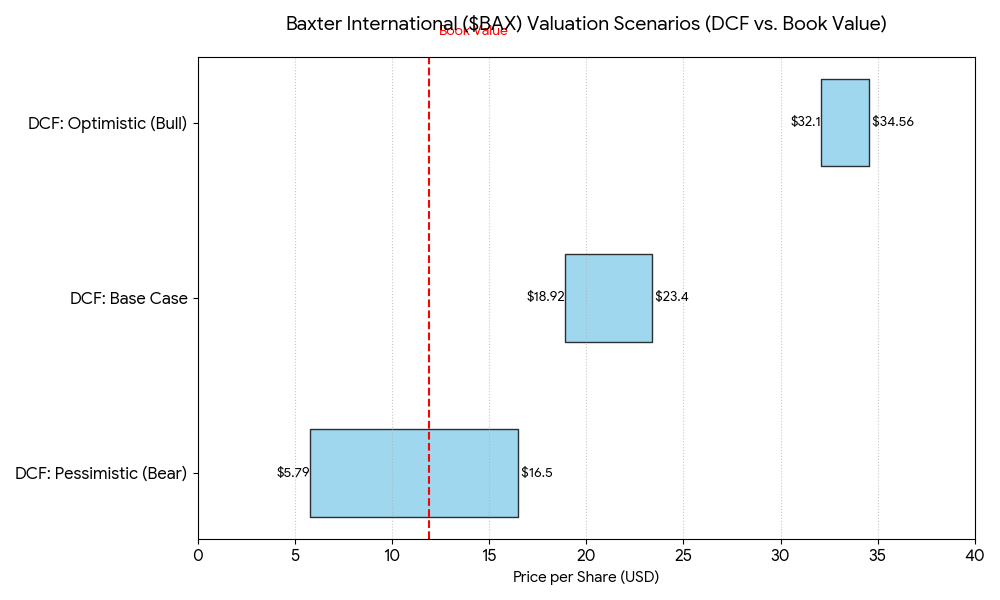

Contextual Insights: The chart above visualizes the various DCF scenarios compared to the current Book Value of $11.92, showing the significant spread between "Bear" and "Bull" expectations.

- DCF Variability: The wide range in the Bear Case ($5.79 to $16.50) reflects extreme scenarios such as a potential "junk" credit rating downgrade and simultaneous failure of the Novum IQ pump resolution*.

- FCF Recovery: Management and analysts anticipate a "back-half weighted" recovery for 2026, meaning most of the projected $700–$800 million in cash will be generated in the third and fourth quarters.

- Book Value vs. Market Price: At a current trading price of approximately $16.15, the stock trades at a Price-to-Book (P/B) ratio of roughly $1.36x to $1.43x, which analysts note is significantly below the MedTech sector median.

* The resolution for the Novum IQ infusion pump platform is a multi-stage process focused on correcting critical software defects that led to five Class I recalls within 14 months of the product's launch. All identified issues are firmware-related rather than hardware-related and Baxter is developing a comprehensive software update designed to address all five recall issues simultaneously.

Despite these risks, the "Margin of Safety" is substantial. Using a base-case DCF model with a 9.5% risk-adjusted WACC, we estimate an intrinsic value of $23.40, offering a 26.9% MOS against the $17.09 trading level. This financial runway, bolstered by cutting the dividend to a nominal $0.01 per quarter, provides the necessary time for operational execution.

Pillar 2: Management

The turnaround’s success hinges on CEO Andrew Hider’s "jockey" performance. Hider possesses an elite "fixer" pedigree, having doubled revenues and tripled the stock price during his tenure at ATS Corporation. However, his "Say-Do" ratio is currently under pressure; Hider’s description of Q4 2025 results as "disappointing" underscores the difficulty of transferring the ATS Business Model (ABM) to a heavily regulated MedTech giant.

Hider is implementing the Baxter GPS (Growth and Performance System) to restore discipline:

- People: Establishing direct P&L responsibility and high-accountability structures.

- Process: Deployment of continuous improvement tools to fix demand planning.

- Performance: Strategic clarity through the removal of the segment management layer.

This "delayering" initiative aims to improve capital allocation precision by embedding R&D and manufacturing directly into business units. Execution risk, however, has been heightened by the March 2026 departure of CFO Joel Grade. The appointment of interim CFO Anita Zielinski occurs just as Baxter faces shareholder investigations into alleged fiduciary breaches, adding a layer of "Governance Uncertainty" that could paralyze decision-making during a critical recovery phase.

Andrew Hider - CEO of ATS Corporation

Andrew Hider served as the CEO of ATS Corporation (formerly ATS Automation Tooling Systems) for approximately 8.5 years.

- Start Date: March 6, 2017

- End Date: August 31, 2025

Tenure Highlights: During his time at ATS, Hider was credited with a massive strategic pivot that analysts now refer to as the "ATS Playbook," which he is currently attempting to replicate at Baxter:

- The Transition: He moved the company away from its heavy reliance on the volatile automotive and energy sectors toward Life Sciences and Food & Beverage, which provided more stable, recurring revenue.

- Stock Performance: Under his leadership, ATS's stock price more than tripled on the Toronto Stock Exchange (TSX).

- Operational Growth: He nearly doubled adjusted revenues over a five-year period (ending 2024) and oversaw more than 20 acquisitions, focusing on "tuck-in" deals that added specific technical capabilities to the ATS portfolio.

- The Exit: His departure was announced in July 2025, and he officially transitioned to Baxter in September 2025, with ATS CFO Ryan McLeod taking over as interim CEO.

| Feature | Past Playbook (ATS & Danaher) | Current Strategy at Baxter (2025–2026+) |

| Operational Framework | ABM (ATS Business Model): A lean manufacturing system based on the Danaher Business System (DBS). | Baxter GPS (Growth and Performance System): A new framework designed to strip out bureaucracy and standardize global operations. |

| Portfolio Focus | High-Growth Automation: Pivoted ATS away from volatile energy/auto sectors toward high-margin Life Sciences. | "New Baxter" Post-Divestiture: Managing the company after the Jan 2025 spinoff of the Kidney Care unit (Vantive). |

| M&A Strategy | Aggressive "Tuck-ins": Dozens of small, high-margin acquisitions (e.g., Avidity Science) to build scale. | Deleveraging First: Shifting from large deals (like Hillrom) to debt repayment, targeting ~3.0x leverage by end of 2026. |

| Product Innovation | Industrial Automation: Focused on digitizing factory floors and robotics. | Connected Care: Integrating Hillrom’s "smart beds" and sensors with AI-driven predictive diagnostics. |

| Leadership Style | Accountability-Driven: Known for a "results-first" style and heavy use of metrics/Master Black Belt principles. | Streamlined Executive Tier: Eliminated the COO role; Hider now directly oversees the core Medical Products segment. |

| Financial Goal | Revenue Multiplier: Doubled adjusted revenue at ATS over five years. | Margin Recovery: Targeting a 100–200 bps operating margin improvement through supply chain optimization. |

Pillar 3: Moat

Baxter’s long-term value is protected by structural assets that are currently masked by operational impairments. The company’s "IV Solutions Moat" is formidable, controlling 60% of U.S. hospital supply. The capital-intensive, FDA-regulated nature of this manufacturing creates a high barrier to entry, preventing commoditization.

However, the IV business is experiencing a "Permanent Reset." Following Hurricane Helene, hospitals implemented fluid conservation protocols (e.g., oral hydration, IV push) now embedded in EHR order sets. Management acknowledges a 10-15% sustained reduction in volume, transforming a once-"sticky" growth driver into a low-growth utility.

The $10.5 billion Hillrom acquisition remains a "problem child." Baxter has already written down 910 million in goodwill** over two years, plus a **290 million write-down of the Welch Allyn brand name. While the "Connected Care" ecosystem (smart beds and patient monitoring) is the intended compounding engine, it is currently an impaired asset requiring aggressive right-sizing.

Competitive Matrix: Strengths vs. Impairments

| Structural Strengths | Current Impairments |

| High Switching Costs: 7-10 year facility standardizations | Class I Recalls: 5 software bugs (2 deaths, 82 injuries) |

| 60% U.S. IV solution market share | IV Reset: 10-15% permanent demand drop |

| Leading Drug Compounding business (+10% growth) | Goodwill Overhang: $1.52B remaining in HS&T |

| Welch Allyn clinical brand trust | Margin Compression: ~900 bps adjusted gross margin drop |

Pillar 4: Catalyst

To avoid becoming a value trap, Baxter requires specific "sparks" to trigger a valuation re-rating.

- Novum IQ Hold Resolution: This is the primary micro-catalyst. Given the severity of the Class I recalls, we anticipate the voluntary ship-hold will last through the entirety of 2026. A resolution would stop the 7-to-10-year loss of market share to competitors like BD Alaris.

- Deleveraging as Re-rating: Achieving the 3.0x net leverage target by end-of-2026 is critical to moving institutional sentiment from "bearish" to "stable."

- Macro Inflection: The "Aging in Place" trend and the move toward "Virtual Hospitals" favor Baxter’s MPT and HST segments. The Connect 360 Vital Signs Monitor serves as the bridge for this high-margin diagnostic data.

The Three Critical "Sparks" for 2026–2027:

- Margin Stabilization: Elimination of stranded costs and manufacturing efficiencies via Baxter GPS.

- Novum Hold Resolution: Recapturing infusion market share once FDA software clearance is achieved.

- TSA Expiration Efficiency: Recapturing logistics and manufacturing margins as Transitional Service Agreements (TSAs) from the Vantive sale roll off in 2025.

Final Verdict: Turnaround or Value Trap

Applying a clinical "Value Trap Check," Baxter BAX$15.92-0.31% remains a viable turnaround candidate:

- Declining Industry? No. Global MedTech demand is robust. Broken Balance Sheet? Improving, though the 3.9x leverage forecast vs. the 3.75x downgrade threshold is the primary risk.

- Lack of Catalysts? No. New leadership and Novum resolution provide a clear roadmap.

- High Valuation? No. 0.8x sales is a generational floor.

Critically, Baxter’s FOCF-to-debt ratio (9-10%) remains weak compared to the 15% peer average, justifying its deep-value status rather than a traditional "buy." The $1.52 billion in remaining goodwill and the $329 million IRS reserve are the final hurdles to a re-rating.

Investment Conclusion: There is a high probability of Baxter reaching a mean valuation of 30-40 per share by 2027, representing a re-rating toward sector medians as leverage hits the 3.0x target. For investors with the stomach for credit-threshold volatility and governance risk, the current price offers a significant margin of safety.