Sector: Consumer Defensive, Industry: Household & Personal Products, Exchange: NYSE

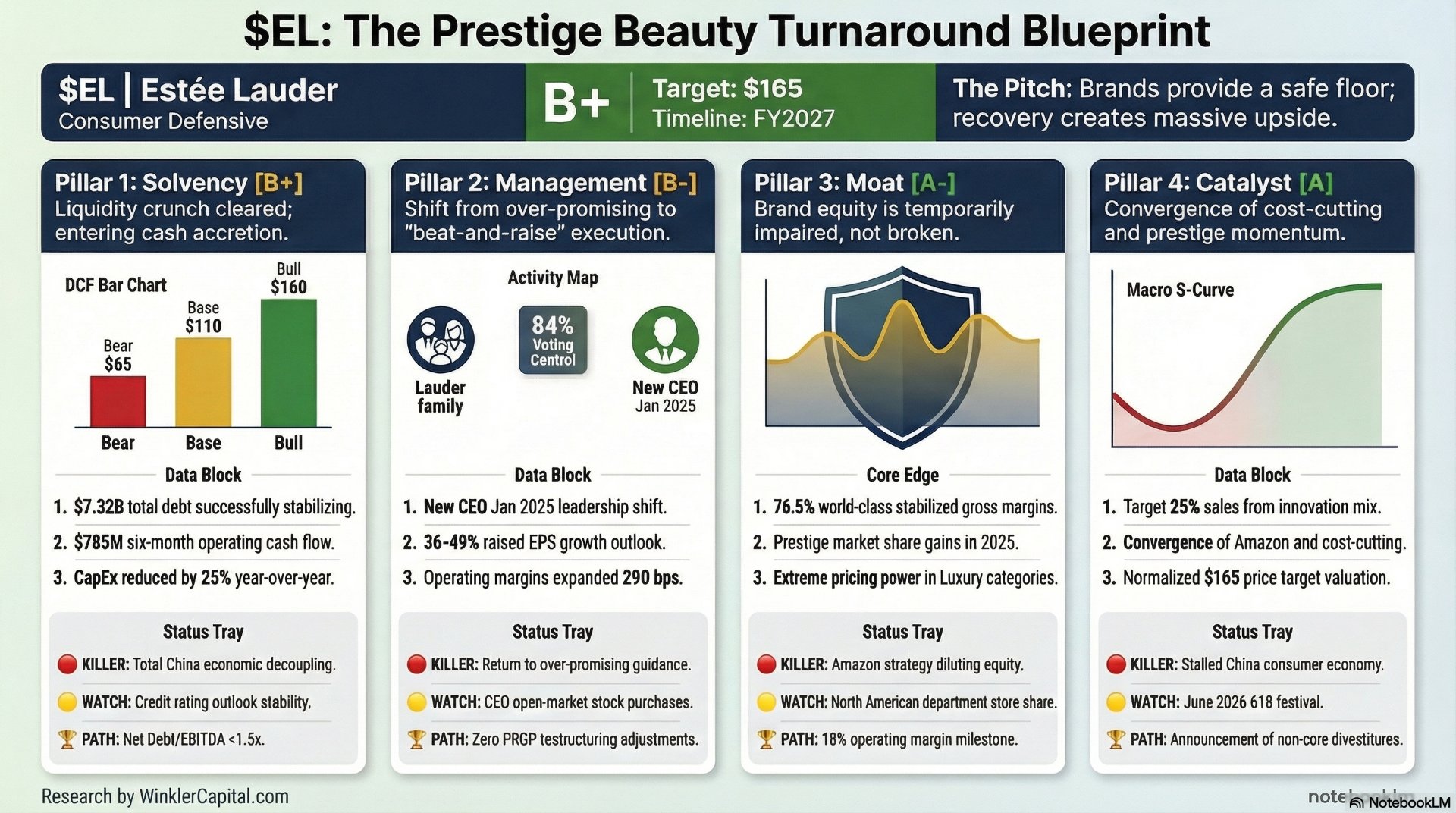

Pillar 1: Solvency (The Foundation)

Grade: B+

- The Floor: EL$68.05-3.76%’s liquidation value is anchored by a premier brand portfolio (La Mer, Estée Lauder, Clinique), which alone would command a massive premium in a private equity or strategic buyout (L'Oréal/LVMH) scenario.

- Triangulated DCF Analysis:

| Scenario | Price Target | Growth Assumption | Core Drivers & Assumptions |

| Bear Case | $65 – $75 | 0% | Permanent loss of China market share; valuation stuck at 18-20x depressed trough earnings. |

| Base Case | $110 – $125 | 2% – 3% (Organic) | Successful PRGP execution; operating margins stabilize at ~12%. |

| Bull Case | $160+ | Double-Digit (EPS) | Reaches 2022-level margins (19%+); full Asia Travel Retail rebound; luxury fragrance scaling. |

- Survival Runway: As of Q2 2026, EL$68.05-3.76% reported $7.32B in total debt. However, operating cash flow for the first six months of FY26 surged to $785M (up from $387M YoY), with CapEx reduced by 25%. Net Debt/EBITDA is stabilizing as EBITDA recovers. Credit ratings remain investment grade (S&P: A- / Moody’s: A2).

- Solvency Risk: NO. The company has successfully navigated the liquidity crunch and is now in a "Cash Accretion" phase.

- Corporate Actions: The dividend remains a priority, signaling management’s confidence in the "Floor."

The Path to A+: Achieve a Net Debt/EBITDA ratio <1.5x while restoring free cash flow conversion to >100% of Net Income, coupled with a credit rating upgrade back to "Stable/Positive" outlook from all major agencies.

Pillar 2: Management (The Jockey)

Grade: B-

- The Say-Do Ratio: After years of over-promising on China’s recovery, under new CEO Stéphane de la Faverie (effective Jan 2025), management finally "kitchen-sinked" guidance in 2025. The Q2 2026 beat-and-raise (raising EPS growth outlook to 36-49%) suggests they are now under-promising and over-delivering.

- Incentive Alignment: The Lauder family still controls ~84% of voting power. While this provides long-term stability, it has historically limited activist intervention. However, the appointment of De La Faverie (an internal veteran with a track record at The Ordinary and Le Labo) aligns with a shift toward high-growth, "nimble" brand management.

- Shareholder Dilution vs. Accretion: Management has paused aggressive buybacks to prioritize the PRGP and debt paydown. Shares outstanding remain stable, but the focus is currently on operational accretion rather than financial engineering.

- Incentive Structure: The "Beauty Reimagined" plan has successfully tied executive bonuses more closely to operating margin expansion and inventory turnover rather than just top-line "vanity" metrics.

The Path to A+: Significant open-market "Skin in the Game" purchases by the new CEO and CFO. A clear transition from "Restructuring Charges" to "Clean Earnings" without the persistent $100M+ quarterly adjustments for the PRGP.

Pillar 3: Moat (The Horse)

Grade: A-

- Profit Margin Trends: Gross margins have stabilized at a world-class 76.5% (Q2 2026). Operating margins expanded 290 bps to 14.4% in the latest quarter. This confirms the moat is temporarily impaired but not permanently broken.

- Structural Advantage: EL$68.05-3.76% possesses "The Luxury Trap." Their brands (Tom Ford, Le Labo) have extreme pricing power. In 2025-2026, they successfully pushed price increases without losing volume in the Fragrance and Hair Care categories.

- Cyclical Durability: Despite a massive drawdown in 2023-2024 due to the China/Travel Retail collapse, the "Lipstick Indicator" held true—consumers traded down in skincare (to EL$68.05-3.76%'s The Ordinary) but stayed within the EL$68.05-3.76% ecosystem. The business remains "sticky," particularly in the prestige tier where EL$68.05-3.76% gained share in the US and China in 2025.

3.1. Profit Margin Trends & Competitive Benchmarking

A comparison with L’Oréal reveals the operational chasm:

| Metric | Estée Lauder (EL$68.05-3.76%) - FY2025 | L’Oréal - FY2025 |

| Sales Growth | -8% (Reported) | +4.0% (Like-for-Like) |

| Gross Margin | 74.0% | 74.3% |

| Operating Margin | Neg. (Impairment Impacted) | 20.2% |

| Dividend Growth | Reduced | +2.9% |

While gross margins are essentially at parity, L’Oréal’s 20.2% operating margin highlights EL$68.05-3.76%’s massive operational inefficiency. EL$68.05-3.76% is losing market share in "Skin Care" and "Makeup" due to poor travel retail conversion, not a collapse in brand equity.

The Path to A+: Reverse the market share losses in North American department stores and prove that the "Amazon Premium Storefront" strategy can scale without diluting brand equity or Gross Margins.

Pillar 4: Catalyst (The Kick)

Grade: A

- Macro Forces: A "normalization" of global travel and a stabilization of the Chinese consumer economy. EL$68.05-3.76% is the purest play on the "Prestige Beauty Recovery."

- Institutional Tailwinds: While not yet a Berkshire-level holding, institutional sentiment shifted in late 2025 as the stock moved from "uninvestable" to a "turnaround play." Activist whispers (Trian/Nelson Peltz) regarding a potential breakup or further portfolio pruning remain a dormant tailwind.

- Micro-Convergence: The convergence of (1) the PRGP cost-cutting, (2) the Amazon distribution launch, and (3) the CEO transition is creating a "Frontside" momentum setup.

- The Momentum Trigger: The Q2 2026 earnings "Beat and Raise" was the primary trigger. The secondary trigger is the 25% innovation mix target for 2026 sales, particularly the upcoming "Double Wear" product refresh.

The Path to A+: A formal announcement of a strategic divestiture of non-core/underperforming brands or a surprise "Aggressive Buyback" program initiated as the debt-to-EBITDA target is met.

4.1. Other Insider Trading - Follow The Whales

Michael Burry - Scion Asset Management "round-trip" trade on The Estée Lauder Companies Inc. (EL$68.05-3.76%) between late 2024 and late 2025.

- The Buy Reason (Value Trap or Bottom Fishing?): In late 2024, EL$68.05-3.76% had crashed 80% from its highs. Burry is a "deep value" investor; he saw a world-class brand (MAC, Clinique, Estée Lauder) trading at a massive discount. He was specifically betting on a China recovery, as EL$68.05-3.76% is the most "China-sensitive" beauty stock in the S&P 500.

- The Sell Reason (The "Macro" Pivot): By mid-2025, the China recovery stalled, and Burry shifted his entire fund into a "crash protection" mode. He sold almost all his long stocks (including EL$68.05-3.76%) to buy Put Options on the S&P 500 and the AI sector. He didn't necessarily stop liking Estée Lauder; he just started hating the direction of the overall market.

Final Verdict: B+ (Strong Buy)

- Primary Risk (The Thesis-Killer): Geopolitical Flare-up in Asia. EL$68.05-3.76% remains heavily over-indexed to China and Travel Retail. A total decoupling or trade war that shuts down high-end imports into Mainland China would result in a permanent loss of capital and break the recovery thesis.

- The original "Thesis-Killer" (failure of PRGP) is being systematically dismantled by actual financial results. With the company on track to reach 15% operating margins, the "valuation gap" with L’Oréal is closing rapidly.

- Monitoring List:

- Mainland China 618 Shopping Festival results (June 2026).

- Inventory Turnover Levels: Must continue to decline to prove "Zero Waste" initiatives are working.

- Amazon Storefront Traction: Direct-to-consumer data from the first full year of the Amazon partnership.

- The Exit Trigger (Summited): Price Target: $165. This represents a return to a 28x P/E multiple on normalized FY27 EPS of $6.00. Exit the position once Operating Margins hit the 18% "Golden Standard" and the market begins to price EL$68.05-3.76% as a "Steady Compounder" rather than a "Turnaround Story."